Things are a little clearer since Mario Draghi’s press conference: the ECB considers the euro’s strength a deflationary risk factor. It is likely to move as a result, albeit in a measured manner starting in June then increasingly so thereafter if necessary, which will probably be the case. Against a backdrop where most other central banks are implementing monetary policies aiming to depreciate their currencies, the hesitancy of the ECB was no longer tenable. So that was a bit of good news but let’s not get ahead of ourselves: by taking such action Mr. Draghi is trying to give the other central banks a taste of their own medicine, making life hard on the Fed, BoJ and BoC, and not the other way around

Author Archives: Véronique Riches-Flores

Productivité, la partie n’est pas gagnée, au contraire des anticipations

La faible croissance de la productivité qui caractérise les années récentes finira-t-elle par laisser place à un rebond structurel, à même de prolonger le cycle présent et d’alimenter la croissance des prochaines années ? C’est bel et bien ce que prédit le consensus, à grand renfort des scénarios de moyen-long termes développés par l’OCDE, le FMI ou autres organismes, tous prometteurs d’un essor considérable de la productivité de l’économie mondiale. Les arguments à l’origine de ces prévisions sont bien connus : abondance des profits des sociétés, révolution scientifique et technologique et gisements de croissance des pays émergents en constituent le fer de lance. L’ensemble permet d’entretenir des anticipations de croissance plus qu’honorables pour l’économie mondiale à horizon 2025 et au-delà et alimente les anticipations sur lesquelles se fondent, pour une large part, la valorisation actuelle des marchés d’actions.

Qu’en est-il au juste ?

Quand les Américains privilégient leur santé, la Fed peut-elle vraiment être satisfaite ?

Au premier trimestre, les Américains ont consacré plus de la moitié de la hausse de leurs dépenses de consommation à leur santé, soit une augmentation de 10 % en rythme annualisé par rapport au trimestre précédent. Sans cette accélération, la consommation réelle des ménages n’aurait pas progressé de 3 % comme publié avant-hier, mais de seulement 1,3 %, quant au produit intérieur brut, il n’aurait pas stagné mais se serait, toutes choses égales par ailleurs, contracté de 1,0 %.

L’analyse détaillée de ces chiffres, vient sans nul doute tempérer le regain d’optimisme consécutif à l’annonce d’une hausse de 4,6 % des dépenses de services au premier trimestre et à la publication du rapport encourageant sur l’emploi du mois d’avril. La Fed ne devrait pas y être hermétique.

With Americans taking care of their health, can the Fed relax?

In the first quarter, Americans allocated over half of the increase in consumption spending to healthcare, which represents an increase of 10% on an annualized basis compared with previous quarter. Without this acceleration, real household consumption would not have increased 3%, as published the day before yesterday, but rather a mere 1.3%; GDP would not have flat-lined but fallen 1.0%, all other variables held constant.

A detailed analysis of these numbers undoubtedly curbs the newfound optimism resulting from the announcement of a 4.6% increase in spending on services in the first quarter and the publication of an encouraging April jobs report. The Fed is not likely to be able to ignore this news.

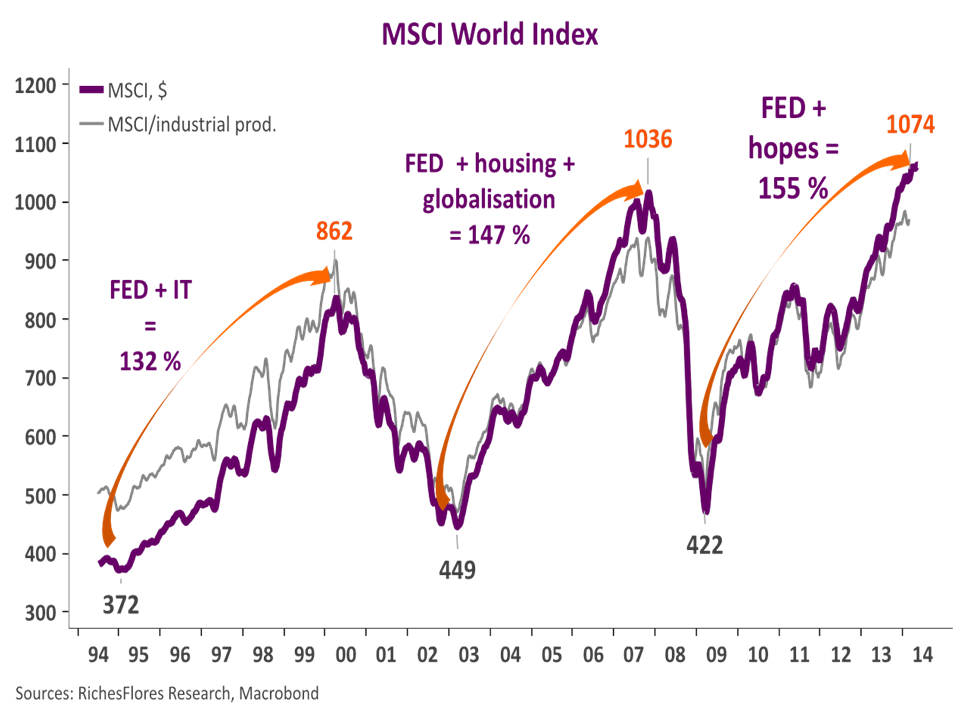

Clouds gathering on risky assets

Our contrarian outlook for a global growth slowdown starting in the second half calls for caution in terms of asset allocation

Global growth slowing next year to 2.8% versus 3.2% this year

- U.S. growth is failing to take off: real estate prices have increased too fast, thus squelching the recovering in the construction industry, growth inertia in services continues to hurt the job market, weak productivity growth has failed to provide the necessary boost to investment that would extend the cycle. Growth disappoints and will not exceed 2% this year or next year.

- Deflation is settling into the euro area and is propagating to the countries in the northern part of the currency union. Following the favorable boost from the economic recovery, keeping the momentum going proves difficult due to the deteriorating export outlook. Germany is not playing its role as an economic engine, other countries are not recovering. Next year, growth will fall to 0.9%, after 1% this year.

- The situation for emerging markets suffers from the negative influence of the Chinese economy: export markets are drying up, soft demand for commodities and devaluation of the Renminbi. Imbalances and chronic shakiness increase the temporary instability. The Russian economy is tipping into a recession, Brazilian growth falls after the uptick from the World Cup, the effects of Indian reforms are diluted by a difficult economic situation.

New bond rally

- The Fed will not see « tapering » through to the end; key rates will stay at zero. The 10Y will decrease to 2-2.25% before the start of 2015.

- The ECB will embark on a long journey of non-conventional monetary policy. Long rates will fall, following the bund, whose 10Y yield will fall to 1-1.25% before early 2015. Interest rate gaps between countries in southern Europe and the German bund will stabilize before widening again in 2015.

- The risk of deflation increases the world over, commodity prices fall back as instability increases. Brent drops to under $90/b.

Growing instability on the forex markets

- The Fed’s strategy shift contradicts the ECB easing, the euro does not fall.

- The BoJ roars back to life after the failure of Abenomics, the yen tumbles in 2015.

- Forex risk increases in EMs, particularly in Asia where the currency war pits the Japanese against the Chinese.

Downturn in the equity markets

The change in outlook weighs on earnings forecasts and cyclical stocks.

The S&P recedes to 1,600, the EuroStoxx returns to 300 points. Industrial equities take a hit, with the DAX squarely in the crosshairs.

Commodities

Has the time come for commodity markets to increase again?

After three years of stagnation, a growing number of investors have been tempted to think so in recent weeks. This renewed interest is hardly surprising given that equity markets are brimming with confidence in the belief that the global economic picture is gradually improving.

Our contrarian economic outlook is naturally quite skeptical of a recovery in global commodity prices. Despite geopolitical and weather-related stress, the international environment runs the risk of suffering a broad downturn amid rampant disinflation and ongoing growth disappointments. Against this backdrop, it would be gold that stands the most likely chance of increasing in value…assuming that long-term real interest rates weaken.

Contents

1. Unusually stable prices since 2012

2. Energy bills generally manageable…

3. … thanks to falling consumption

4. Keeping an eye on agriculture…

5. Precious metals: end of QE could trigger a rise…

Moniteur des matières premières

Le temps est-il venu d’une reprise sur les marchés des matières premières ?

Après trois années d’inertie, nombreux sont les investisseurs tentés de le penser ces dernières semaines. Conforme au schéma d’une amélioration graduelle de la situation économique internationale, ce regain d’intérêt n’est, somme toute, guère surprenant au vue de la confiance affichée par les marchés d’actions.

Notre scénario économique contrariant laisse, lui, peu de place à une reprise des cours mondiaux. Aux tensions géopolitiques ou climatiques près, l’environnement international pourrait même signaler un risque de décrue généralisée dans un contexte de désinflation rampante et de déceptions persistantes sur la croissance. Dans un tel contexte, c’est du côté de l’or que pourraient se trouver les fondamentaux les plus persuasifs d’un changement de cap possible à la hausse des cours…

Sommaire

- Stabilité peu coutumière des cours depuis 2012

- Une facture énergétique globalement supportable…

- … Grâce au repli de la consommation

- Veille agricole…

- Précieux : un ressaisissement possible avec la fin de QE

Schizophrénie obligataire

Monteront, monteront pas ? L’incertitude sur l’évolution à venir des taux d’intérêt à long terme n’en finit pas, et l’impatience grandit, avec, toutefois, ce paradoxe : la crainte d’être surpris par une chute intempestive des marchés obligataires (soit une envolée des taux longs), face au désir contradictoire, de pouvoir, enfin, envisager une remontée de ces mêmes taux, qui viendrait signer une amélioration définitive des perspectives économiques. Alors que ces incertitudes animent le marché américain depuis déjà près d’un an, moment à partir duquel la Fed a laissé entendre une possible fin du QE, voilà que la Banque du Japon s’inquiète de l’absence de prise en considération du changement de contexte inflationniste du pays par le marché obligataire japonais, se disant préoccupée du risque que représenterait un réveil tardif de ce dernier. De tels commentaires ne manquent pas de surprendre…