Download the Full Article

Those who believe we can offset the devastating effect of an overvalued euro by copying German recipes from the preceding decade are kidding themselves.

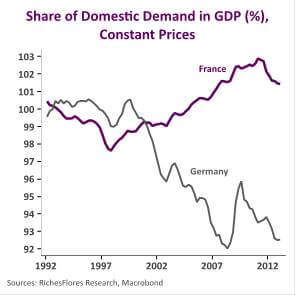

In fact, a brief look at how the German economy achieved competitive adjustment will highlight the unique conditions that supported such a turnaround. The international environment in the first decade of this century not only proved extremely beneficial to Germany’s industrial recovery; it also made the turnaround fairly painless for the country’s consumers.

Today, no other eurozone Member State has anywhere near the kind of industrial strength enjoyed by Germany, or for that matter the means to ease the social pain of the reforms needed to put the common currency area back on a competitive footing. If Europe’s leaders persist in copying past German recipes without considering how or why they worked, the monetary union will unquestionably be facing its greatest danger ever.

To fend off that danger, there is just one viable response: an orchestrated depreciation of the euro along the lines of the 1985 Plaza Accord, which was designed to counteract the damaging effects of an overvalued dollar on the world economy. Let’s hope the prospects of a protracted eurozone slump will win enough converts to such an approach, because it probably holds out the last chance to save the common currency.