When it was announced that U.S. weekly jobless claims fell again, it immediately overshadowed the much less positive 1% fall in Q1 GDP. A drop in unemployment claims continues to be seen as a signal that the job market and, along with it, consumption are improving. This lends credence to the idea that the GDP drop in the first quarter was a mere blip on the radar and did not reflect the reality of the American situation: The idea being to look ahead and not back. We have a considerably different interpretation of this data; our take on the jobs figures is significantly less upbeat. Here are two reasons to not take for granted the markets’ renewed optimism in recent days.

Archives par catégories : GLOBAL MACRO

Day to day Global Macro Context Analysis

Clouds gathering on risky assets

Our contrarian outlook for a global growth slowdown starting in the second half calls for caution in terms of asset allocation

Global growth slowing next year to 2.8% versus 3.2% this year

- U.S. growth is failing to take off: real estate prices have increased too fast, thus squelching the recovering in the construction industry, growth inertia in services continues to hurt the job market, weak productivity growth has failed to provide the necessary boost to investment that would extend the cycle. Growth disappoints and will not exceed 2% this year or next year.

- Deflation is settling into the euro area and is propagating to the countries in the northern part of the currency union. Following the favorable boost from the economic recovery, keeping the momentum going proves difficult due to the deteriorating export outlook. Germany is not playing its role as an economic engine, other countries are not recovering. Next year, growth will fall to 0.9%, after 1% this year.

- The situation for emerging markets suffers from the negative influence of the Chinese economy: export markets are drying up, soft demand for commodities and devaluation of the Renminbi. Imbalances and chronic shakiness increase the temporary instability. The Russian economy is tipping into a recession, Brazilian growth falls after the uptick from the World Cup, the effects of Indian reforms are diluted by a difficult economic situation.

New bond rally

- The Fed will not see « tapering » through to the end; key rates will stay at zero. The 10Y will decrease to 2-2.25% before the start of 2015.

- The ECB will embark on a long journey of non-conventional monetary policy. Long rates will fall, following the bund, whose 10Y yield will fall to 1-1.25% before early 2015. Interest rate gaps between countries in southern Europe and the German bund will stabilize before widening again in 2015.

- The risk of deflation increases the world over, commodity prices fall back as instability increases. Brent drops to under $90/b.

Growing instability on the forex markets

- The Fed’s strategy shift contradicts the ECB easing, the euro does not fall.

- The BoJ roars back to life after the failure of Abenomics, the yen tumbles in 2015.

- Forex risk increases in EMs, particularly in Asia where the currency war pits the Japanese against the Chinese.

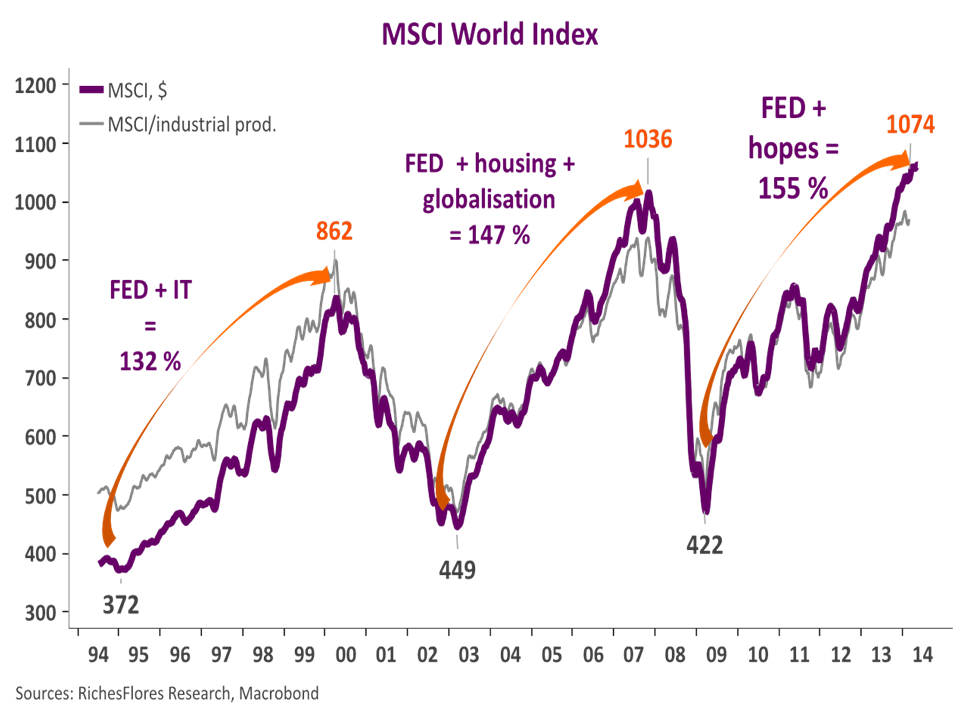

Downturn in the equity markets

The change in outlook weighs on earnings forecasts and cyclical stocks.

The S&P recedes to 1,600, the EuroStoxx returns to 300 points. Industrial equities take a hit, with the DAX squarely in the crosshairs.

Commodities

Has the time come for commodity markets to increase again?

After three years of stagnation, a growing number of investors have been tempted to think so in recent weeks. This renewed interest is hardly surprising given that equity markets are brimming with confidence in the belief that the global economic picture is gradually improving.

Our contrarian economic outlook is naturally quite skeptical of a recovery in global commodity prices. Despite geopolitical and weather-related stress, the international environment runs the risk of suffering a broad downturn amid rampant disinflation and ongoing growth disappointments. Against this backdrop, it would be gold that stands the most likely chance of increasing in value…assuming that long-term real interest rates weaken.

Contents

1. Unusually stable prices since 2012

2. Energy bills generally manageable…

3. … thanks to falling consumption

4. Keeping an eye on agriculture…

5. Precious metals: end of QE could trigger a rise…

Global investment: lingering disappointment

The improvement in the global economic backdrop since late 2013 has not provided the desired results when it comes to investment. Although the European recovery has shown a few positive signs, an overview of global investment trends continues to paint a disappointing picture:

- In the U.S., where recent corporate earnings and leading indicators have fallen short of expectations;

- In Japan, where the 2013 rally remains highly dependent on companies’ export performance, which has become somewhat of a mixed bag;

- In the emerging world, where many Asian countries are confronted with excess capacities, at a time when most big countries are now paying the price for their structural shortcomings;

- In Europe, where – unlike the rest of the world – leading indicators are actually encouraging: could the region rise to the challenge? Of course, such a scenario is unrealistic

The extended absence of an improvement in investment prospects is one the most troubling constraint for future economic development. We discuss this topic in further detail in « Investment inertia: what is at stake« .

China: desperately seeking growth drivers

How bad has the Chinese economy gotten to warrant such a firm reaction by Chinese authorities in recent weeks?

Since mid-January, the People’s Bank of China has orchestrated a 3% fall in the yuan. Our suspicions of a shift in currency policy are being confirmed and if such a move was intended to spark volatility to discourage capital inflows the strategy has certainly been successful. And the movement could well continue because China seems to be in disarray as it faces a major problem: mopping up excess private debt in the economy while maintaining growth. It is a tall task and growing evidence suggests that the 2014 GDP growth target of 7.5% is becoming less and less credible.

What kind of message are bonds markets sending?

Since the Fed began to taper in January, yields on 10-year government bonds have fallen across the board: 25 basis points in the U.S., nearly 80bp in Spain, 65bp in Italy and 30bp in Germany. Even the poor news from the latest FOMC held on Wednesday only had a marginal effect on 10Y yields in the U.S., which finished trading yesterday at 2.77%, i.e. where they were some ten days ago.

None of this resembles the generally-accepted scenario about what would happen when the Fed began to change course on quantitative easing. In fact, the consensus was that the taper would trigger a sharp increase in long-term interest rates in the western world. This simply hasn’t played out. Why? And what should be made of it?

The Fed’s big bet

With thirteen of its sixteen members believing that monetary tightening would be appropriate starting in 2015 and ten of those believing that the level of the Fed Funds will be greater or equal to 1% at the end of next year, the message delivered by the Fed following its meeting on March 18th and 19th breaks with its past communication. Standing in stark contrast with the bond market’s current anticipations, this shift is liable to trigger sharp reactions, which is troubling for a variety of reasons:

– for the capital markets, first, the distinct possibility that interest rates and the equity markets in the US and elsewhere in the world will overreact to this shift in tone;

– for the US economy, second, whose robustness is unclear and ability to deal with more expensive credit even more uncertain;

– and for emerging markets and the countries of southern Europe, lastly, who are exposed to the increasing risk of capital flight.

The appreciating euro or the competitive deflation trap

You heard it here first: the euro would not drop versus the dollar and could even increase. And here we are. During trading yesterday, the euro flirted with USD 1.40, its highest level since October 2011 after gaining in excess of 7% since the start of the year. This is a worrying development, which could erase nearly all of the support that improving global conditions have provided to exports.

Two reasons explain why our forecasts, unlike the market consensus, never strayed from the EUR 1.40/euro exchange rate in the past two years:

• the first is rooted in our skepticism with regard to 1) the consensus that the US economy is presumably in good health and 2) anticipations that the Fed would normalize its monetary policy in response to the expected improvement.

• the second is grounded in the side effects of the competitive deflation policies carried out by the EMU countries. The shrinking inflation gap between the euro area and the rest of the world, resulting from these policies, protects the currency’s purchasing power. Consequently, these policies offer de facto support to the euro, particularly versus the greenback whose value is automatically diluted by the massive scale of pump priming in recent years.

Therefore, it is hardly surprising that the recent disappointments on American growth have pushed the euro higher, especially since the ECB dashed all hopes of additional monetary easing last week.